Choosing between an IRA and a 401(k) for retirement savings can feel overwhelming. Both offer tax advantages and the potential for significant growth, but their structures and eligibility requirements differ significantly. This comparison explores the key distinctions between traditional and Roth versions of each, examining contribution limits, investment options, tax implications, and accessibility to help you make an informed decision.

Understanding the nuances of each plan is crucial for maximizing your retirement savings. Factors such as your income, age, risk tolerance, and employer-sponsored plan availability will all influence which plan, or combination of plans, best aligns with your financial goals. We’ll delve into these factors, providing clear explanations and examples to guide you through this important financial choice.

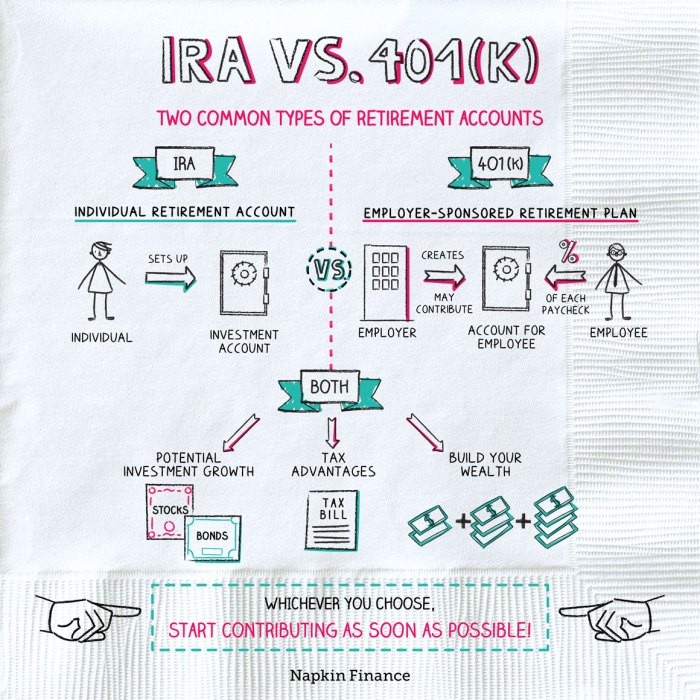

Introduction to IRA and 401(k) Plans

Retirement planning is crucial, and Individual Retirement Accounts (IRAs) and 401(k) plans are two popular vehicles to help you save for your future. Understanding their differences and features is key to making informed decisions about your retirement savings strategy.Both IRAs and 401(k)s are retirement savings plans designed to provide tax advantages. However, they differ significantly in their structure, contribution limits, and investment options.

This section will clarify the fundamental characteristics of each.

IRA and 401(k) Plan Definitions

An IRA, or Individual Retirement Account, is a retirement savings account that offers tax advantages. Contributions may be tax-deductible (Traditional IRA) or grow tax-free (Roth IRA). A 401(k) plan, on the other hand, is a retirement savings plan sponsored by an employer. Employees contribute a portion of their pre-tax salary, and often the employer matches a percentage of those contributions.

Similar to IRAs, 401(k) plans can be either traditional or Roth.

Traditional vs. Roth: IRA and 401(k) Differences

The primary difference between traditional and Roth versions lies in when taxes are paid. With a traditional IRA or 401(k), contributions are typically tax-deductible, meaning you reduce your taxable income in the current year. However, withdrawals in retirement are taxed as ordinary income. Conversely, Roth IRAs and 401(k)s involve after-tax contributions, meaning you don’t get an immediate tax deduction.

However, qualified withdrawals in retirement are tax-free. The choice between traditional and Roth depends on your current and projected future tax brackets. If you expect to be in a higher tax bracket in retirement, a Roth account might be more beneficial. If you anticipate a lower tax bracket in retirement, a traditional account might be preferable.

Contribution Limits for 2024

Contribution limits for both IRAs and 401(k)s are adjusted annually. For 2024, the maximum contribution to a traditional or Roth IRA is $7,000 for those under age 50. Those age 50 and older can contribute an additional $1,000, bringing the total to $8,000. For 401(k) plans, the maximum employee contribution for 2024 is $23,000 for those under age 50, with an additional $7,500 catch-up contribution allowed for those age 50 and older, resulting in a maximum contribution of $30,500.

Employer matching contributions are in addition to these limits. It is important to note that these limits can change annually, so it is crucial to check the most up-to-date information from the IRS.

Illustrative Examples of Retirement Planning

Understanding the potential growth of IRA and 401(k) contributions is crucial for effective retirement planning. The following scenarios illustrate how these plans can accumulate wealth over time, depending on factors like contribution amount, investment growth rate, and time horizon.

Retirement Planning for a Young Professional

Let’s consider Sarah, a 25-year-old who starts contributing to both an IRA and a 401(k). She contributes the maximum allowed to her IRA ($6,500 in 2023, assuming she doesn’t qualify for the catch-up contribution) and $23,000 to her 401(k) annually. We’ll assume an average annual investment return of 7%, a reasonable long-term expectation based on historical market performance, although past performance is not indicative of future results.

This return is not guaranteed. We will also assume consistent contributions for simplicity.

| Year | IRA Contribution | IRA Balance (End of Year) | 401(k) Contribution | 401(k) Balance (End of Year) |

|---|---|---|---|---|

| 1 | $6,500 | $6,500 | $23,000 | $23,000 |

| 10 | $6,500 | $86,180 | $23,000 | $332,557 |

| 20 | $6,500 | $205,774 | $23,000 | $1,029,737 |

| 30 | $6,500 | $436,778 | $23,000 | $2,807,757 |

These figures demonstrate the power of compounding returns and early saving. Note that taxes and fees are not included in this simplified example. Actual returns will vary.

Retirement Planning for an Individual Closer to Retirement

Now, let’s consider David, a 55-year-old who has been contributing to a 401(k) for many years but has a smaller IRA. He has $200,000 in his 401(k) and $50,000 in his IRA. He plans to retire in 10 years. He continues to contribute the maximum to his 401(k) and his IRA, taking advantage of the catch-up contributions allowed for those age 50 and older.

We will again assume a 7% annual return, recognizing that this is not guaranteed.

The catch-up contributions can significantly boost retirement savings in later years.

| Year | IRA Contribution | IRA Balance (End of Year) | 401(k) Contribution | 401(k) Balance (End of Year) |

|---|---|---|---|---|

| 1 | $7,500 | $57,825 | $30,000 | $236,750 |

| 10 | $7,500 | $122,253 | $30,000 | $462,634 |

David’s example highlights the importance of continued contributions even closer to retirement, along with the benefits of catch-up contributions. Again, this is a simplified example and actual returns may vary. It’s important to consult with a financial advisor for personalized retirement planning.

Ultimately, the “best” retirement savings plan depends entirely on your individual circumstances. While 401(k)s often offer employer matching contributions and higher contribution limits, IRAs provide flexibility and portability. A well-rounded retirement strategy may even incorporate both. By carefully considering your income, age, risk tolerance, and investment goals, you can create a personalized plan that maximizes your savings and sets you up for a comfortable retirement.

Remember to consult with a qualified financial advisor for personalized guidance.

Clarifying Questions

Can I contribute to both an IRA and a 401(k)?

Yes, provided you meet the income requirements for IRA contributions and your employer offers a 401(k) plan.

What happens to my 401(k) if I change jobs?

You generally have the option to leave your 401(k) with your previous employer, roll it over into a new employer’s plan, or roll it over into an IRA.

Are there income limits for contributing to a Roth IRA?

Yes, there are income limits for contributing to a Roth IRA. If your income exceeds these limits, you may not be able to contribute the full amount or may be ineligible.

What are the penalties for early withdrawal from an IRA or 401(k)?

Early withdrawals are generally subject to income tax and a 10% penalty unless certain exceptions apply (e.g., first-time homebuyer, qualified education expenses).