Securing a comfortable retirement requires careful planning and a thorough understanding of both personal savings and Social Security benefits. This exploration delves into the intricacies of retirement planning, examining the various vehicles available for accumulating savings, the complexities of Social Security eligibility and benefit calculations, and strategies for managing financial resources throughout retirement. We’ll navigate the challenges of inflation, explore diverse investment approaches, and ultimately, empower you to build a secure financial future.

From understanding the eligibility criteria for Social Security to optimizing your retirement savings through 401(k)s and IRAs, we’ll cover essential aspects of retirement planning. This includes developing a realistic retirement budget, mitigating investment risks, and coordinating Social Security benefits with other income streams to achieve your desired lifestyle in retirement. We aim to provide practical guidance and clear explanations to simplify the often-complex process of securing your financial well-being.

Managing Retirement Savings

Successfully navigating retirement requires careful management of your savings. This involves understanding and mitigating investment risks, diversifying your portfolio, strategically withdrawing funds, and accounting for the persistent threat of inflation. Proper planning in these areas can significantly impact your financial security throughout your retirement years.

Managing Investment Risk During Retirement

Managing investment risk during retirement is crucial because your savings are no longer replenished by active income. A common strategy is to shift towards a more conservative investment approach as you approach and enter retirement. This often involves reducing exposure to higher-risk assets like stocks and increasing holdings in lower-risk, more stable investments such as bonds or money market accounts.

The goal is to balance the need for growth with the preservation of capital. For example, a retiree might gradually reduce their stock allocation from 70% to 40% over several years, reinvesting the proceeds into less volatile options. The specific allocation will depend on individual circumstances, risk tolerance, and the length of retirement.

Diversification in a Retirement Portfolio

Diversification is a fundamental principle of sound investment management, especially in retirement. It involves spreading your investments across different asset classes (stocks, bonds, real estate, etc.) and sectors to reduce the impact of any single investment performing poorly. A diversified portfolio is less susceptible to significant losses from market fluctuations or economic downturns. For instance, if the technology sector experiences a downturn, a portfolio heavily invested in technology stocks will suffer more than a diversified portfolio that also includes investments in healthcare, consumer goods, and government bonds.

A well-diversified portfolio aims to minimize overall portfolio volatility and enhance long-term returns.

Strategic Withdrawal Methods from Retirement Accounts

Strategic withdrawal from retirement accounts is essential for ensuring your funds last throughout retirement. Common methods include systematic withdrawals, which involve regularly withdrawing a fixed amount or a percentage of your portfolio’s value. Another approach is the “bucket” strategy, which divides retirement savings into several accounts with different levels of risk and liquidity. For instance, one bucket might contain highly liquid assets to cover immediate expenses, while another holds long-term investments for future needs.

The choice of withdrawal method depends on factors like your lifespan expectancy, spending habits, and risk tolerance. Consider consulting a financial advisor to determine the best strategy for your individual circumstances.

Impact of Inflation on Retirement Savings and Income

Inflation erodes the purchasing power of money over time. This means that the same amount of money will buy fewer goods and services in the future than it does today. Inflation significantly impacts retirement savings and income because it reduces the real value of your accumulated wealth and your retirement income. For example, if inflation is 3% annually, a $50,000 annual retirement income will only have the purchasing power of approximately $48,500 in a year, and even less in subsequent years.

To mitigate the impact of inflation, retirees should consider investing in assets that tend to keep pace with or outpace inflation, such as inflation-protected securities or real estate, and adjust their withdrawal strategies accordingly. Regularly reviewing and adjusting your retirement plan to account for inflation is crucial to maintaining your standard of living throughout retirement.

Retirement Planning and Social Security Coordination

Effective retirement planning requires a comprehensive understanding of how Social Security benefits interact with your personal savings and other income streams. Failing to account for Social Security can lead to inaccurate retirement income projections and potentially insufficient funds to maintain your desired lifestyle during retirement. This section explores how to integrate Social Security into your overall retirement strategy.

Social Security’s Impact on Retirement Planning Strategies

Social Security benefits significantly influence retirement planning. The amount you receive depends on your earnings history and the age at which you begin collecting benefits. Early retirement typically results in lower monthly payments, while delaying benefits increases them. This decision profoundly impacts the overall retirement income projection, influencing how much you need to save from other sources to achieve your desired financial security.

For example, someone planning to retire at 62 might need to save more aggressively than someone who delays benefits until age 70. Understanding the trade-offs between early access to benefits and higher lifetime payments is crucial for optimizing your retirement plan.

Coordinating Social Security Benefits with Other Retirement Income Sources

Successfully coordinating Social Security with other retirement income sources, such as 401(k)s, IRAs, pensions, and part-time work, is key to a comfortable retirement. A holistic approach is necessary. For instance, if your Social Security benefits cover a significant portion of your essential expenses, you might be able to draw less aggressively from your personal savings, preserving capital for unexpected expenses or leaving a legacy.

Conversely, if Social Security provides minimal income, you’ll need a larger nest egg from other sources. Careful budgeting and financial projections, considering all income streams, are essential for a comprehensive plan.

Estimating Total Retirement Income

Estimating total retirement income involves projecting your Social Security benefits and your income from other sources. The Social Security Administration’s website provides tools to estimate your future benefits based on your earnings history. For your personal savings, you can use online retirement calculators or consult a financial advisor. These tools allow you to input various factors, such as your current savings, expected investment returns, and planned withdrawal rate, to create a comprehensive projection.

For example, suppose your estimated Social Security benefit is $20,000 annually and your projected income from personal savings is $30,000 annually; your total estimated retirement income would be $50,000. However, it’s crucial to remember that these are estimates and unforeseen circumstances could affect the actual amount.

Checklist for Coordinating Social Security Benefits with Retirement Planning

Proper coordination requires a systematic approach. Here’s a checklist to guide you:

- Obtain a Social Security benefits statement to understand your estimated future payments.

- Determine your desired retirement lifestyle and associated expenses.

- Estimate your retirement income from all sources, including Social Security, pensions, 401(k)s, IRAs, and other investments.

- Analyze the gap between your estimated income and expenses. If there’s a shortfall, adjust your savings plan or retirement age.

- Consult with a financial advisor to develop a comprehensive retirement plan.

- Regularly review and adjust your plan as your circumstances change.

- Consider the impact of inflation on your retirement expenses and adjust your plan accordingly.

The Impact of Inflation on Retirement Savings

Inflation silently erodes the purchasing power of money over time. This is a crucial factor to consider when planning for retirement, as the value of your savings today will likely be less in the future if inflation is not accounted for. Understanding the effects of inflation and implementing strategies to mitigate its impact is essential for securing a comfortable retirement.Inflation’s effect on retirement savings is a reduction in their real value.

Essentially, your savings will buy you less in the future than they do today. This means that the same amount of money will purchase fewer goods and services as prices rise. The longer you are in retirement, the more significant this erosion of purchasing power can become. Failing to account for inflation can lead to a shortfall in your retirement funds, potentially jeopardizing your financial security.

Strategies for Protecting Retirement Savings from Inflation

Several strategies can help protect your retirement savings from the ravages of inflation. Diversification across various asset classes is key. Investing in assets that historically outpace inflation, such as stocks and real estate, is a common approach. These investments tend to increase in value at a rate that at least keeps pace with, or ideally exceeds, inflation. However, it’s crucial to remember that these investments also carry a higher degree of risk.

A balanced approach, considering your risk tolerance and time horizon, is essential. Regularly rebalancing your portfolio ensures that your asset allocation remains aligned with your goals and risk profile.

Adjusting Retirement Withdrawals for Inflation

Adjusting retirement withdrawals to account for inflation is crucial for maintaining a consistent standard of living throughout retirement. Simply withdrawing the same dollar amount each year will lead to a gradual decline in purchasing power. A common strategy is to increase annual withdrawals by a percentage that approximates the expected inflation rate. This ensures that your withdrawals maintain their real value over time.

For example, if inflation is projected at 3%, increasing your withdrawal amount by 3% annually helps offset the impact of rising prices.

Examples of Inflation’s Impact on Retirement Plans

A retiree who planned to withdraw $50,000 annually from their savings might find that $50,000 only buys the equivalent of $40,000 worth of goods and services after ten years of 2% annual inflation.

Imagine a couple who retired in 2000 with $500,000 in savings. If inflation averaged 3% annually, the real value of their savings would be significantly less by 2023. They might find that their savings have less purchasing power than initially anticipated, necessitating adjustments to their spending or requiring them to work longer.

Retirement Planning

Planning for retirement is crucial for securing financial stability and maintaining your desired lifestyle in your later years. A well-defined retirement plan allows you to anticipate and address potential financial challenges, ensuring a comfortable and fulfilling retirement. Failing to plan adequately can lead to significant financial hardship and compromise your quality of life.

The Importance of Early Retirement Planning

Beginning your retirement planning early offers significant advantages. The power of compounding returns on investments allows your savings to grow exponentially over time. Starting early allows you to invest smaller amounts regularly, achieving the same or greater results than investing larger sums later in life. Furthermore, early planning allows for greater flexibility in adjusting your plan to account for unexpected life events or changes in financial circumstances.

Delaying retirement planning reduces your ability to take advantage of these benefits and increases the pressure to save larger amounts later, potentially affecting other financial goals.

Key Factors to Consider When Creating a Retirement Plan

Several key factors influence the success of a retirement plan. These include determining your retirement income needs, estimating your retirement expenses, assessing your current savings and assets, and choosing appropriate investment strategies. Understanding your risk tolerance and time horizon is also crucial in making sound investment decisions. Finally, considering the impact of inflation on your savings and adjusting your plan accordingly is vital to maintain purchasing power throughout retirement.

A Step-by-Step Guide to Developing a Comprehensive Retirement Plan

Developing a comprehensive retirement plan involves a structured approach. First, estimate your retirement expenses, considering factors like housing, healthcare, travel, and leisure activities. Next, assess your current savings and assets, including retirement accounts, investments, and property. Then, determine the gap between your projected expenses and your accumulated savings. This gap represents the amount you need to save before retirement.

Finally, create a savings plan, outlining your contributions to retirement accounts and investments, and regularly review and adjust your plan as needed to account for changes in your circumstances or financial goals. Consider consulting with a financial advisor for personalized guidance.

Tips for Staying on Track with a Retirement Plan

Maintaining a consistent approach is crucial for retirement planning success.

- Regularly review and adjust your plan to account for life changes and economic conditions.

- Automate your savings contributions to ensure consistent investments.

- Diversify your investment portfolio to manage risk effectively.

- Seek professional financial advice to gain personalized guidance and support.

- Track your progress regularly and make adjustments as needed to stay on track.

Retirement Savings

Securing a comfortable retirement requires diligent planning and consistent saving. Understanding various savings methods, the advantages of early contributions, and the different retirement account options available are crucial steps in building a financially secure future. This section will Artikel these key aspects of retirement savings.

Methods for Saving for Retirement

Several methods exist for accumulating retirement funds. These approaches vary in their tax advantages, contribution limits, and investment options. Careful consideration of individual financial circumstances and risk tolerance is essential when selecting a savings strategy.

Benefits of Early Retirement Savings

Starting to save early offers significant advantages due to the power of compound interest. Even small, regular contributions made early in one’s career can accumulate substantially over time, leading to a larger retirement nest egg compared to starting later. This is because the interest earned on your initial investments also earns interest, creating a snowball effect. For example, investing $100 per month at age 25 versus age 45 can yield a dramatically different balance by retirement age, assuming similar returns.

Types of Retirement Accounts

Several types of retirement accounts cater to diverse saving needs and preferences. Each offers distinct tax benefits and investment choices.

- 401(k) plans: Employer-sponsored plans that often include matching contributions, offering tax advantages on contributions and earnings until retirement.

- Traditional IRAs: Individual Retirement Accounts that allow pre-tax contributions, reducing current taxable income. Taxes are paid upon withdrawal in retirement.

- Roth IRAs: IRAs where contributions are made after tax, but withdrawals in retirement are tax-free.

- SEP IRAs: Simplified Employee Pension plans, designed for self-employed individuals and small business owners.

- 403(b) plans: Retirement savings plans for employees of public schools and certain non-profit organizations.

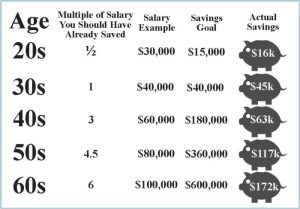

Calculating Retirement Savings Needs

Estimating retirement savings needs requires considering various factors, including desired lifestyle, expected lifespan, and inflation. A common approach involves projecting annual expenses in retirement and adjusting for inflation over the retirement period. The following table provides a simplified example:

| Age | Annual Expenses (Current Dollars) | Annual Expenses (Adjusted for Inflation) | Total Savings Needed (Estimate) |

|---|---|---|---|

| 65 | $50,000 | $50,000 | (See Calculation Below) |

| 70 | $50,000 | $57,000 (assuming 1.4% annual inflation) | (See Calculation Below) |

| 75 | $50,000 | $65,000 (assuming 1.4% annual inflation) | (See Calculation Below) |

| 80 | $50,000 | $74,000 (assuming 1.4% annual inflation) | (See Calculation Below) |

Calculation Example: Assuming a 25-year retirement and a 4% annual withdrawal rate, the total savings needed at age 65 would be approximately $50,000

– 25 / 0.04 = $3,125,000. This is a simplified calculation and doesn’t account for potential investment growth or unexpected expenses.

Note: This is a simplified example and does not consider factors such as investment returns, taxes, or healthcare costs. Professional financial advice is recommended for personalized retirement planning.

Planning for retirement is a journey that requires foresight, diligence, and a well-defined strategy. By understanding the intricacies of Social Security benefits, diversifying your investment portfolio, and proactively managing your savings, you can build a strong foundation for a secure and fulfilling retirement. Remember, early planning and consistent contributions are key to achieving your financial goals. This comprehensive guide serves as a starting point, encouraging you to seek personalized financial advice to tailor your plan to your unique circumstances and aspirations.

FAQ Summary

What is the full retirement age for Social Security benefits?

The full retirement age for Social Security benefits depends on your birth year and gradually increases. You can find your specific full retirement age on the Social Security Administration website.

Can I withdraw from my 401(k) before retirement without penalty?

Early withdrawals from a 401(k) are generally subject to penalties and taxes unless specific exceptions apply, such as hardship withdrawals. Consult a financial advisor for guidance.

How does inflation affect my retirement savings?

Inflation erodes the purchasing power of your savings over time. To mitigate this, consider investing in assets that can keep pace with or outpace inflation.

What are the differences between a traditional IRA and a Roth IRA?

A traditional IRA offers tax deductions on contributions, while a Roth IRA provides tax-free withdrawals in retirement. The best choice depends on your current and projected tax bracket.