Securing a comfortable retirement is a paramount goal for many, and the choice between a pension and a 401(k) plan often stands as a critical juncture in this journey. Understanding the nuances of each plan – their funding mechanisms, investment strategies, tax implications, and inherent risks – is essential for making an informed decision aligned with individual financial circumstances and long-term objectives.

This exploration delves into the key distinctions between these two prevalent retirement vehicles, equipping readers with the knowledge to navigate this important financial decision.

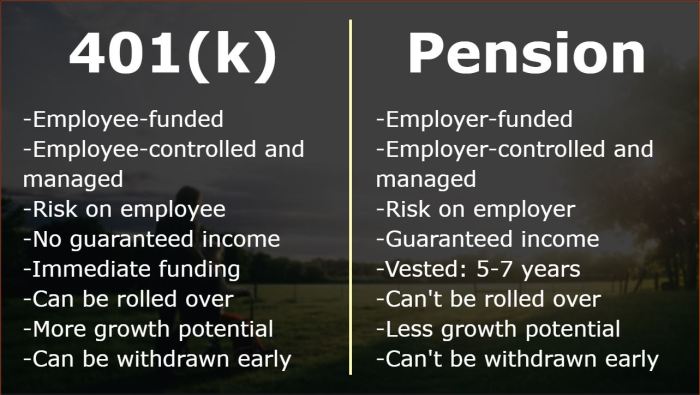

Both pensions and 401(k)s offer pathways to retirement savings, but their structures and risk profiles differ significantly. Pensions, often provided by employers, offer a defined benefit, guaranteeing a specific income stream upon retirement. Conversely, 401(k)s are defined contribution plans, where the final payout depends on contributions, investment performance, and market fluctuations. This fundamental difference underscores the need for careful consideration of individual risk tolerance and long-term financial planning strategies.

Risk and Security

Choosing between a pension and a 401(k) involves carefully considering the inherent risks and the level of security each offers. Both plans present different exposure to market fluctuations and offer varying degrees of protection against unforeseen circumstances. Understanding these differences is crucial for making an informed retirement planning decision.

Risk Associated with Pensions and 401(k)s

Pensions, traditionally defined benefit plans, generally bear less investment risk for the employee. The employer assumes the responsibility for managing the investments and guaranteeing a specific level of retirement income. However, the risk of employer insolvency exists; if the company goes bankrupt, pension payments may be reduced or cease entirely, depending on the plan’s funding and the existence of a Pension Benefit Guaranty Corporation (PBGC) safety net.

In contrast, 401(k) plans, defined contribution plans, place the investment risk squarely on the employee. Investment returns depend entirely on market performance, meaning the employee’s retirement savings are vulnerable to market volatility and downturns. While diversification can mitigate some risk, there’s no guarantee of a specific income level in retirement.

Security and Protection Offered

The security offered by pensions and 401(k)s differs significantly. Pensions provide a guaranteed income stream, at least to a certain extent, provided the sponsoring employer remains solvent. The PBGC offers some protection against complete loss in the event of employer insolvency, although the guaranteed benefits are often less than the promised amount. 401(k) plans offer less inherent security.

The value of the retirement savings is directly tied to market performance and is susceptible to losses during economic downturns. However, the employee retains control over their investments and can choose a more conservative investment strategy to minimize risk. Protection mechanisms such as diversification and employer-sponsored matching contributions can enhance the security of a 401(k).

Impact of Inflation

Inflation significantly erodes the purchasing power of both pension payouts and 401(k) withdrawals. For pensions, the fixed payout amount may not keep pace with rising prices, reducing the real value of the retirement income over time. For example, a $2,000 monthly pension payment might only buy $1,500 worth of goods and services in ten years due to inflation.

Similarly, inflation impacts 401(k) withdrawals. If the investment returns don’t outpace inflation, the real value of the accumulated savings decreases, potentially leaving retirees with less purchasing power than anticipated. Consider the scenario where someone withdraws $100,000 from their 401(k) and inflation rises 3% annually; the purchasing power of that $100,000 would be substantially lower in the future.

Downsides and Limitations

Pensions have limitations such as potential loss of benefits due to employer insolvency and the lack of flexibility in managing investments. Payouts are often fixed and may not adjust to individual needs or changing circumstances. 401(k) plans, on the other hand, offer greater investment control but require active participation and financial literacy. Market downturns can significantly impact savings, and the responsibility for successful retirement planning rests solely with the employee.

Additionally, there’s no guaranteed income stream, and longevity risk (living longer than anticipated) can deplete savings.

Retirement Planning and Savings Strategies

Planning for retirement requires a multifaceted approach, strategically combining various savings vehicles to ensure a comfortable financial future. Both pensions and 401(k)s play significant roles, but their integration within a broader retirement strategy is crucial for maximizing benefits and mitigating risks. Diversification across multiple investment options further strengthens this plan, providing resilience against market fluctuations.

Integrating Pensions and 401(k)s into a Retirement Plan

A comprehensive retirement plan often involves a combination of guaranteed income streams, such as pensions, and growth-oriented investments, like 401(k)s. Pensions provide a predictable, regular income stream, offering financial security during retirement. 401(k)s, on the other hand, offer the potential for greater growth but also carry higher investment risk. Ideally, a well-structured plan leverages the stability of a pension to cover essential living expenses while utilizing the 401(k) to supplement income and potentially enhance retirement lifestyle.

The proportion allocated to each depends on individual circumstances, risk tolerance, and the size of the pension benefit. For instance, someone with a generous pension might allocate a smaller portion to their 401(k), focusing more on preserving capital, while someone with a smaller pension might prioritize aggressive growth within their 401(k).

The Importance of Diversifying Retirement Savings

Diversification is key to managing risk within a retirement portfolio. Relying solely on one investment vehicle exposes retirees to significant financial vulnerability should that investment underperform. Diversification across different asset classes (stocks, bonds, real estate, etc.) and investment vehicles (401(k), IRA, Roth IRA, annuities) helps mitigate risk. For example, a downturn in the stock market might negatively impact a 401(k) but might not significantly affect a bond-heavy portfolio or a pension.

This approach significantly reduces the impact of market volatility on overall retirement savings.

Estimating Retirement Income

Estimating retirement income involves projecting both pension payouts and 401(k) withdrawals. Pension payouts are typically fixed and easily calculable using information provided by the pension plan administrator. Estimating 401(k) withdrawals requires more careful consideration. A common approach involves using a withdrawal rate, often between 3% and 5% annually, based on the expected lifespan of retirement and the desired level of risk.

For example: A retiree with a $2,000 monthly pension and a $500,000 401(k) might estimate annual 401(k) withdrawals at 4% ($20,000). This, combined with the annual pension income ($24,000), would provide an estimated annual retirement income of $44,000. This calculation, however, is an estimate and doesn’t account for inflation or unexpected expenses.

Developing a Personalized Retirement Savings Plan

Developing a personalized retirement savings plan is a multi-step process.

- Determine Retirement Goals: Define your desired lifestyle and spending during retirement. Consider factors like travel, healthcare, hobbies, and housing costs.

- Estimate Retirement Expenses: Calculate your anticipated monthly and annual expenses in retirement, factoring in inflation.

- Assess Current Savings: Determine your current savings in all retirement accounts (401(k), IRA, pensions, etc.).

- Calculate Savings Gap: Compare your estimated retirement expenses to your projected retirement income (from pensions and estimated 401(k) withdrawals). This difference represents the savings gap you need to address.

- Develop a Savings Strategy: Create a plan to bridge the savings gap, including adjusting savings rates, investing strategies, and potentially delaying retirement.

- Regularly Review and Adjust: Periodically review your plan, adjusting it as needed to account for changes in income, expenses, market conditions, and personal circumstances.

Illustrative Examples

Choosing between a pension and a 401(k) depends heavily on individual circumstances and risk tolerance. Let’s examine scenarios where each plan shines, and how they can complement each other.

Pension Plan as the Most Suitable Option

A scenario where a pension plan is most suitable involves a long-tenured employee of a stable, large organization offering a generous defined benefit pension. Imagine Sarah, a teacher with 30 years of service in a public school system. Her pension plan guarantees a specific monthly income upon retirement, adjusted for inflation. This predictable income stream provides significant security, mitigating the risk associated with market fluctuations that impact 401(k)s.

Her employer’s contributions are substantial, requiring minimal personal contributions from her. This predictability is especially valuable given the relatively lower salary often associated with public sector jobs.

401(k) Plan as the Most Suitable Option

Conversely, a 401(k) plan becomes the most suitable option for individuals with a longer time horizon, higher risk tolerance, and a desire for greater control over their retirement savings. Consider Mark, a software engineer at a tech startup. His company offers a 401(k) with employer matching, but no pension. Mark is young, and his career trajectory suggests potential for significant income growth.

He can contribute aggressively to his 401(k), taking advantage of tax advantages and potentially achieving higher returns through investments in stocks and other higher-growth assets. The higher risk associated with this strategy aligns with his longer time horizon and ability to withstand potential market downturns.

Combining Pension and 401(k) for Retirement Security

Let’s examine how a hypothetical individual, let’s call her Jessica, might combine both plans. Jessica works for a mid-sized company that offers both a defined contribution pension plan (a less generous version of a traditional pension) and a 401(k) with employer matching. Jessica contributes the maximum amount allowed to her 401(k) to maximize the employer match, and also takes advantage of the company’s pension plan.

The pension provides a guaranteed base income, while the 401(k) offers the potential for higher growth to supplement her retirement income. This strategy balances security with the potential for increased returns, providing a more robust retirement nest egg.

Visual Representation of Pension vs. 401(k) Growth

Imagine two lines on a graph representing the growth of a pension and a 401(k) over 30 years. The pension line shows a steady, upward incline, reflecting consistent growth at a predetermined rate, representing a relatively low-risk investment with predictable returns. The 401(k) line, however, is more volatile. Under favorable market conditions, it shows a steep, upward trajectory, reflecting significant growth.

However, during periods of market downturn, the line dips significantly, illustrating the risk associated with market-based investments. In a scenario with moderate market performance, the 401(k) line shows a moderate, but still less predictable, incline compared to the pension. Over the long term, the 401(k) might surpass the pension in value under positive market conditions, but carries the risk of lower returns under less favorable circumstances.

The pension remains a constant, predictable source of income regardless of market fluctuations.

Ultimately, the optimal choice between a pension and a 401(k) hinges on a comprehensive assessment of individual circumstances, risk appetite, and retirement goals. While pensions provide the security of guaranteed income, 401(k)s offer greater control and flexibility over investments. A well-informed decision, incorporating careful consideration of tax implications and potential market volatility, is crucial for building a secure and fulfilling retirement.

Understanding the strengths and weaknesses of each plan empowers individuals to create a personalized retirement strategy that aligns with their unique financial landscape and aspirations.

Essential FAQs

What happens to my 401(k) if my employer goes bankrupt?

Your 401(k) assets are generally protected from employer bankruptcy. They are held in a separate trust and are considered your personal property.

Can I withdraw from my 401(k) before retirement?

Early withdrawals are generally subject to penalties and taxes, unless specific exceptions apply (e.g., hardship withdrawals).

What is the difference between a traditional and Roth 401(k)?

Traditional 401(k)s offer tax-deferred growth, while Roth 401(k)s provide tax-free withdrawals in retirement.

Are there contribution limits for 401(k)s?

Yes, annual contribution limits are set by the IRS and can change yearly.

Can I roll over my 401(k) into an IRA?

Yes, you can generally roll over your 401(k) into an IRA upon leaving your employer, though specific rules apply.