Securing a comfortable retirement requires careful planning and a proactive approach to saving. However, many individuals unknowingly make critical mistakes that can significantly impact their financial well-being in their later years. Understanding and avoiding these common pitfalls is crucial for building a secure and fulfilling retirement. This guide explores key areas where missteps often occur, offering practical strategies to help you navigate the complexities of retirement savings effectively.

From the insidious erosion of savings due to inflation to the risks of insufficient diversification and the consequences of premature withdrawals, we will examine a range of potential problems. We will also delve into the importance of realistic budgeting, adapting investment strategies over time, and the often-overlooked aspect of comprehensive estate planning. By understanding these challenges and implementing the suggested solutions, you can significantly improve your chances of achieving your retirement goals.

Ignoring Inflation’s Impact on Savings

Planning for retirement requires careful consideration of various factors, and one often overlooked element is the insidious effect of inflation. Failing to account for inflation can significantly diminish the real value of your retirement savings, leaving you with less purchasing power than anticipated. Understanding and addressing this is crucial for a comfortable retirement.Inflation erodes the purchasing power of money over time.

This means that the same amount of money will buy you fewer goods and services in the future than it does today. This is because the general price level of goods and services increases due to various economic factors. For example, if the inflation rate is 3%, a product costing $100 today will likely cost $103 next year.

Over time, this seemingly small increase compounds, leading to a substantial reduction in your savings’ real value. This is particularly critical for long-term savings like retirement funds, where the impact of inflation can be felt most acutely over decades.

Adjusting Savings Goals for Inflation

To counteract inflation’s impact, it’s essential to adjust your savings goals to account for projected inflation rates. This involves estimating future costs and increasing your savings accordingly. One common method is to use a projected inflation rate to inflate your future retirement spending needs. For instance, if you estimate needing $50,000 annually in retirement in 20 years and expect an average annual inflation rate of 2%, you’ll need to save significantly more than $50,000 to maintain that same purchasing power.

You can use online inflation calculators or financial planning software to project future values and adjust your savings targets. Alternatively, a more conservative approach might involve using a higher inflation rate than projected to create a safety margin. This approach acknowledges the uncertainty inherent in long-term inflation predictions.

Inflation’s Impact on Savings Over 20 Years

The following table illustrates the difference between the nominal (stated) value of savings and the real (inflation-adjusted) value over a 20-year period, considering different inflation scenarios. We assume a fixed initial savings amount of $100,000.

| Year | Nominal Value | Inflation Rate | Real Value |

|---|---|---|---|

| 0 | $100,000 | – | $100,000 |

| 10 | $100,000 | 2% | $82,035 |

| 10 | $100,000 | 3% | $74,409 |

| 20 | $100,000 | 2% | $67,297 |

| 20 | $100,000 | 3% | $55,368 |

| 20 | $100,000 | 4% | $45,639 |

Note: The real value is calculated by discounting the nominal value back to present value using the given inflation rate. This table demonstrates how a seemingly small difference in the inflation rate can significantly impact the real value of your savings over time. For example, with 4% inflation, the real value of $100,000 after 20 years is only $45,639.

This highlights the critical importance of incorporating inflation into your retirement planning.

Not Adjusting Investment Strategy Over Time

Maintaining a static investment strategy throughout your retirement journey can significantly impact your financial security. As your circumstances and goals evolve, so too should your approach to investing. Failing to adapt your strategy risks underperforming, leaving you with insufficient funds to meet your retirement needs.Your investment strategy should be a dynamic tool, not a rigid plan. As retirement nears, the focus shifts from aggressive growth to preserving capital and generating a steady income stream.

This transition requires a careful and considered shift in asset allocation, moving away from higher-risk, higher-reward investments towards those offering stability and predictable returns.

Asset Allocation Shifts Towards Retirement

The process of shifting asset allocation involves gradually reducing exposure to equities (stocks) and increasing holdings in fixed-income securities (bonds), as well as potentially exploring other income-generating assets. This reduces the volatility of your portfolio, minimizing the risk of significant losses close to or during retirement. A gradual approach minimizes the impact of market fluctuations and allows for a smoother transition.

For example, someone in their 50s might aim to gradually reduce their equity allocation by 5-10% annually, reinvesting those funds into bonds or other lower-risk investments.

Investment Strategies Across Retirement Stages

Understanding the different investment needs across various retirement stages is crucial for effective financial planning. Strategies should adapt to changing circumstances and priorities.

- Pre-Retirement (Ages 40-60s): This stage emphasizes growth. A higher allocation to equities (stocks) is appropriate, allowing for significant capital appreciation. Diversification across different asset classes, including international stocks and real estate, is important to mitigate risk. Consider also incorporating some fixed-income investments to balance the portfolio and provide some stability. For example, a 60/40 portfolio (60% stocks, 40% bonds) might be suitable, although the specific allocation depends on individual risk tolerance and time horizon.

- Early Retirement (Ages 60-75): During early retirement, the focus shifts to preserving capital while generating income. The equity allocation should be reduced, with a greater emphasis on fixed-income investments such as bonds, certificates of deposit (CDs), and annuities. Dividend-paying stocks can also provide a consistent income stream. A potential portfolio might consist of 40% stocks, 50% bonds, and 10% in alternative investments like real estate or precious metals, depending on individual preferences and risk tolerance.

- Late Retirement (Ages 75+): In late retirement, preserving capital and ensuring a stable income stream become paramount. Risk tolerance is often lower, necessitating a portfolio heavily weighted towards low-risk, income-generating assets like government bonds, high-yield savings accounts, and annuities. A portfolio might consist of 20% stocks, 70% bonds, and 10% cash or equivalents. Regular withdrawals need to be carefully managed to ensure the portfolio’s longevity.

Ignoring Estate Planning

Failing to plan for the distribution of your assets after your death can create significant complications for your loved ones and potentially lead to unintended tax consequences. Proper estate planning ensures a smooth transfer of your assets according to your wishes, minimizing stress and potential legal battles for your heirs. It’s a crucial element of securing your financial legacy.Estate planning involves various legal tools designed to manage the distribution of your assets after you pass away.

Choosing the right tools depends on the complexity of your assets, family dynamics, and your specific goals for asset distribution. Careful consideration of these factors is essential to creating a plan that effectively protects your assets and meets your wishes.

Estate Planning Tools and Their Implications

A well-structured estate plan typically incorporates several key components. Understanding the purpose and implications of each is crucial for making informed decisions.

- Wills: A will is a legal document that Artikels how you want your assets distributed after your death. It names an executor to manage the process and specifies beneficiaries for your property, ensuring it goes to the intended recipients. Without a will (dying “intestate”), the state dictates how your assets are distributed, which may not align with your wishes.

- Trusts: Trusts provide more control and flexibility than wills. A trust involves transferring assets to a trustee, who manages them for the benefit of beneficiaries. Different types of trusts (e.g., revocable, irrevocable) offer varying levels of control and tax advantages. For example, a living trust allows you to manage assets during your lifetime and specify how they are distributed after your death, potentially avoiding probate.

- Beneficiary Designations: These are crucial for assets held in retirement accounts (IRAs, 401(k)s), life insurance policies, and other accounts. Designating beneficiaries directly on these accounts bypasses probate and ensures the assets go directly to the intended recipients, streamlining the process and avoiding potential delays. Failure to name beneficiaries can lead to lengthy legal battles and unintended consequences.

Steps to Effective Estate Planning

Creating a comprehensive estate plan requires a methodical approach. Consider these steps to ensure a well-structured and legally sound plan:

- Inventory Your Assets: Begin by creating a detailed list of all your assets, including real estate, bank accounts, investments, and personal property. This provides a clear picture of your estate’s value and complexity.

- Determine Your Goals: Define your objectives for asset distribution. Who are your intended beneficiaries? Do you have specific wishes regarding the distribution of certain assets? Clearly outlining your goals is essential for creating a plan that reflects your desires.

- Choose Your Estate Planning Tools: Based on your goals and asset complexity, select the appropriate tools (will, trust, beneficiary designations). Consider seeking professional advice from an estate planning attorney to determine the best approach for your situation.

- Consult with Professionals: An estate planning attorney can guide you through the process, ensuring your plan is legally sound and compliant with all relevant laws. A financial advisor can help you assess your financial situation and integrate your estate plan with your overall financial goals. A tax advisor can help minimize tax implications.

- Review and Update Regularly: Life circumstances change, and your estate plan should reflect these changes. Review and update your plan periodically, especially after significant life events such as marriage, divorce, birth of a child, or major asset acquisitions or disposals. This ensures your plan remains current and aligns with your evolving needs.

Failing to Utilize Employer-Sponsored Retirement Plans

Employer-sponsored retirement plans, such as 401(k)s and 403(b)s, offer significant advantages for building a secure retirement. These plans provide a convenient and often tax-advantaged way to save for the future, and many employers offer matching contributions, essentially giving you free money towards your retirement. Ignoring these plans represents a substantial missed opportunity to enhance your long-term financial well-being.Participating in employer-sponsored retirement plans offers several key benefits.

Firstly, contributions are often tax-deferred, meaning you don’t pay income taxes on the money until you withdraw it in retirement. This allows your savings to grow tax-free for many years. Secondly, many employers offer matching contributions, essentially adding to your savings at no extra cost to you. This is a powerful incentive to participate and can dramatically accelerate the growth of your retirement nest egg.

Finally, these plans provide a structured and automated way to save, making it easier to consistently contribute to your retirement goals.

Employer Matching Contributions and Retirement Savings Growth

Employer matching contributions can significantly boost retirement savings. Many employers match a percentage of employee contributions, often up to a certain limit. For example, an employer might match 50% of your contributions up to 6% of your salary. This means if you contribute 6% of your salary, your employer will contribute an additional 3%, effectively doubling your contribution.

This free money dramatically increases the overall growth of your retirement savings.

Illustrative Example of Retirement Savings Growth

Let’s illustrate the potential impact of employer matching contributions on retirement savings over a 30-year period. We’ll assume an annual contribution of $5,000, a 7% annual rate of return, and a 50% employer match up to 6% of salary (in this example, let’s assume the $5000 represents 6% of the salary).

| Year | Savings Without Match (7% return) | Savings With Match (7% return) | Difference |

|---|---|---|---|

| 1 | $5,350 | $7,500 | $2,150 |

| 10 | $79,500 | $120,000 | $40,500 |

| 20 | $212,000 | $325,000 | $113,000 |

| 30 | $480,000 | $740,000 | $260,000 |

Note: This is a simplified example and does not account for factors such as taxes, fees, or changes in investment performance. Actual results may vary. The figures illustrate the substantial long-term benefits of employer matching. The significant difference in savings between the scenarios with and without employer matching highlights the importance of participating in these plans. Taking advantage of employer matching is essentially like getting a guaranteed return on your investment before any market fluctuations even occur.

Retirement Planning and Retirement Savings

Retirement planning and retirement savings are intrinsically linked; one cannot effectively exist without the other. A robust savings plan is the foundation upon which a successful retirement is built, but without a comprehensive plan outlining goals, timelines, and risk tolerance, even the most diligent saving may fall short. This interconnectedness highlights the need for a holistic approach, integrating financial goals with personal aspirations for a fulfilling retirement.

Creating a Comprehensive Retirement Plan

A well-structured retirement plan acts as a roadmap, guiding your financial decisions and ensuring you’re on track to achieve your retirement objectives. Failing to create such a plan leaves your financial future vulnerable to unforeseen circumstances and market volatility. A comprehensive plan should incorporate several key elements.

- Define Retirement Goals: Clearly articulate your vision for retirement. What lifestyle do you envision? Where do you want to live? What activities will you pursue? Quantify these aspirations; for example, “Maintain a lifestyle requiring $60,000 annual income” or “Travel internationally for three months each year.” This quantification provides a concrete target for your savings.

- Determine Your Time Horizon: Establish a realistic timeframe for retirement. Consider your current age, desired retirement age, and any potential early retirement scenarios. A longer time horizon generally allows for more aggressive investment strategies, while a shorter horizon necessitates a more conservative approach.

- Calculate Savings Needs: Based on your goals and time horizon, estimate the total amount you’ll need to save. Consider factors such as inflation, healthcare costs, and potential longevity. Online retirement calculators can assist with this process, but professional financial advice is often beneficial for complex scenarios. For example, if you aim for a $60,000 annual income in retirement, and expect to live for 20 years post-retirement, you’ll need to save approximately $1.2 million, assuming a conservative 3% annual return on investments.

- Develop an Investment Strategy: Choose investments that align with your risk tolerance, time horizon, and savings goals. This might involve a diversified portfolio including stocks, bonds, and real estate. Consider seeking professional advice from a financial advisor to develop a suitable asset allocation strategy.

- Incorporate Estate Planning: Plan for the distribution of your assets after your death. This includes creating a will, establishing trusts, and designating beneficiaries for your retirement accounts. Proper estate planning ensures your assets are distributed according to your wishes and minimizes potential tax burdens for your heirs.

Regular Review and Adjustment of the Retirement Plan

Life is unpredictable. Job changes, unexpected expenses, market downturns, and changes in personal circumstances can all significantly impact your retirement plan. Therefore, regular review and adjustment are crucial. Annual reviews are recommended, allowing you to monitor progress, assess the impact of market fluctuations, and make necessary adjustments to your savings and investment strategies. For example, if market conditions change significantly, you may need to rebalance your portfolio to maintain your desired level of risk.

Similarly, a major life event like a marriage or the birth of a child might necessitate recalculating your savings needs and adjusting your investment timeline. Professional financial advice can be invaluable during these review periods.

Successfully navigating the path to a financially secure retirement requires a multifaceted approach, encompassing careful planning, diligent saving, and a proactive management of your investments. By avoiding the common mistakes discussed – from neglecting inflation’s impact to overlooking estate planning – you can substantially increase your chances of achieving your financial aspirations. Remember that regular review and adjustment of your retirement plan are vital to ensure it remains aligned with your evolving needs and market conditions.

Proactive planning empowers you to build a confident and comfortable future.

Quick FAQs

What is the best way to diversify my retirement portfolio?

A diversified portfolio typically includes a mix of asset classes such as stocks, bonds, and real estate, with the specific allocation depending on your risk tolerance and time horizon. Consider consulting a financial advisor for personalized guidance.

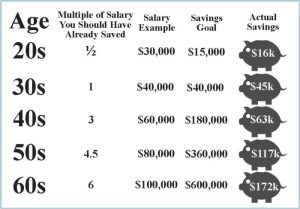

How much should I be saving for retirement?

The ideal savings amount depends on your lifestyle, desired retirement income, and expected lifespan. A general guideline is to aim for saving at least 10-15% of your pre-tax income, but it’s best to create a personalized retirement budget.

What are the tax implications of withdrawing from my retirement accounts early?

Early withdrawals often incur significant tax penalties and may reduce your Social Security benefits. Consult a tax professional for detailed information relevant to your specific situation.

When should I start planning for retirement?

The sooner you begin planning, the better. Even small contributions early on can grow significantly over time due to compounding interest. It’s never too early, or too late, to start.